Posted June 24, 2026

By Sean Ring

The Skunk at the Garden Party

Nobody invited the skunk.

But Jamie Dimon brought it anyway.

Two Mondays ago at that den of iniquity, the Council on Foreign Relations, the CEO of the world’s largest bank walked into a room full of the global establishment and told them their precious party is built on sugar… and the hangover is going to be nasty.

Dimon dispensed with the usual corporate reassurance. He pissed on their parade.

Numb on record highs and wafer-thin credit spreads, Wall Street missed the whole thing.

Sugar High

Dimon said, “The U.S. economy is right now running on a sugar high.”

That’s not the sanitized version that made it into the financial press.

This particular sugar high has three ingredients. First, government deficits are running at roughly 6.5% of GDP… not during wartime or in crisis mode—just peacetime on a Wednesday. Second, past stimulus is still sloshing through the system like the punch bowl the Fed didn’t take away. Third, the private credit market has grown so fast and so loose that the people running it have, in Dimon’s words, “completely lost touch with reality.”

Combine those three, and you get what looks like a strong economy. Strong earnings. Low unemployment. And consumers are still spending.

You also get prosperity… borrowed from the future. That growth was purchased, not earned. The economy looks healthy until the bill arrives.

The Skunk

Dimon says the bill is inflation.

“The real skunk at the garden party is going to be inflation, which is going to creep back up. The gravity of interest rates hasn’t gone anywhere.”

This matters because the entire market narrative of the past two years rests on one assumption: the Fed won the inflation fight, and easier money is coming. Stocks are priced for it. Credit spreads are priced for it. The private credit boom is priced for it.

Dimon is telling you that assumption is wrong.

Deficits of 6.5% of GDP are inflationary. Full stop. Reshoring is inflationary. Rearmament is inflationary. Energy underinvestment is inflationary. All of these forces are pushing prices higher, slowly and persistently, regardless of what last month’s CPI print said.

The Fed can declare victory, but the math doesn’t care.

Schroedinger’s Credit Cycle

“Massive government deficits and booming private credit markets have created an environment where players have completely lost touch with reality. A market that hasn’t seen a real credit cycle in forever breeds a complacency that never ends well.”

The current generation of credit professionals has never experienced a full-on crisis. They went through the government-mandated private-sector shutdown of 2020-2021, Jay Powell’s 2022 rate shock, and the 2023 minor banking scare, but the Fed quickly intervened in those kerfuffles. They’ve never been through the kind of credit deterioration that would’ve taught them what risk actually costs.

That inexperience, combined with a flood of private credit chasing yield, has produced a market in which the price of risk is absurdly low. Relative to the actual level of risk in the system.

Dimon runs stress tests across extreme scenarios: high rates, oil shocks, geopolitical blowups. He doesn’t forecast. He prepares. The rest of the market is still using the forecast.

M&A Rant

“You sit in these endless executive meetings, and the first thing management does when they can’t drive organic growth is start pitching M&A. I don’t want to hear that bullshit.”

His words, not mine… though I wish they were.

When companies can’t grow organically, their underlying businesses are struggling. The honest response is to fix it. The lazy response is to buy something, call it a strategic acquisition, collect a bonus, and let the next CEO deal with the mess of integrating the acquired business into the old firm.

Dimon has watched this movie for 30 years. He knows how it ends. Most M&A destroys shareholder value. Most of it gets done anyway because it rewards the people who pitch it.

And he said that in a room full of the people who pitch it.

Debt Reckoning

“I’m pessimistic we’re going to solve our debt problem until there’s a crisis.”

A man with more access to policymakers than almost anyone alive doesn’t believe DC will fix the debt problem on its own.

He went further.

“I hope it’s a mild crisis, but it will happen one day. And the bond vigilantes will be back, and everyone will act surprised, and we’ll have to do something.”

Bond vigilantes. That phrase hasn’t been part of mainstream conversation since the 1990s, when rising deficits drove Treasury yields up and forced fiscal discipline on the Clinton White House. James Carville once said he wanted to be reincarnated as a bond trader because then he could intimidate everybody.

The vigilantes went dormant for 30 years. The Fed kept rates low. Foreign buyers kept showing up at auctions.

Dimon is telling you that era is ending.

He said when the vigilantes return, the adjustment won’t be gentle. It will be forced, fast, and painful, arriving on a timeline no one can predict.

Skin in the Game

An X post that summarized Dimon’s remarks made an apt connection to Nassim Taleb’s “skin in the game” framework.

Taleb’s point is simple. People who bear no personal cost for being wrong will always underestimate risk. They reach for the comforting forecast. They prefer the elegant model to the messy reality. They collect their speaking fee regardless of the outcome.

Dimon has skin in the game. His reputation, institution, and legacy ride on whether his risk management works when the cycle turns. That produces a different kind of honesty than you get from the economist who packs up and flies home after his speech, whether or not his predictions hold up.

The complacency Dimon warns about is the rational behavior of people who don’t pay a price when they’re wrong.

That’s why he said it out loud, at the CFR, on the record.

Dimon knows most of the room won’t believe him until they have to.

Wrap Up

The economy is on a sugar high. Inflation is coming back. The credit cycle will return. The bond vigilantes are resting, not gone. DC won’t fix the debt until a crisis forces it.

I didn’t say that. Jamie Dimon did.

None of this requires panic. It requires honesty.

Own real assets (even if it’s not necessarily gold and silver at this moment). Own cash flows tied to physical reality. Keep dry powder in the form of cash and T-bills. Reduce exposure to narratives that assume the next decade will look like the last one.

The skunk has been spotted.

The only question is how long before the other guests notice the smell.

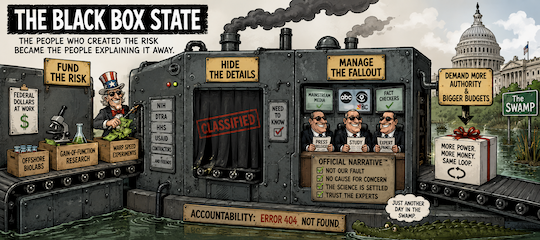

Black Box State

Posted June 23, 2026

By Sean Ring

Financial Fathers

Posted June 19, 2026

By Sean Ring

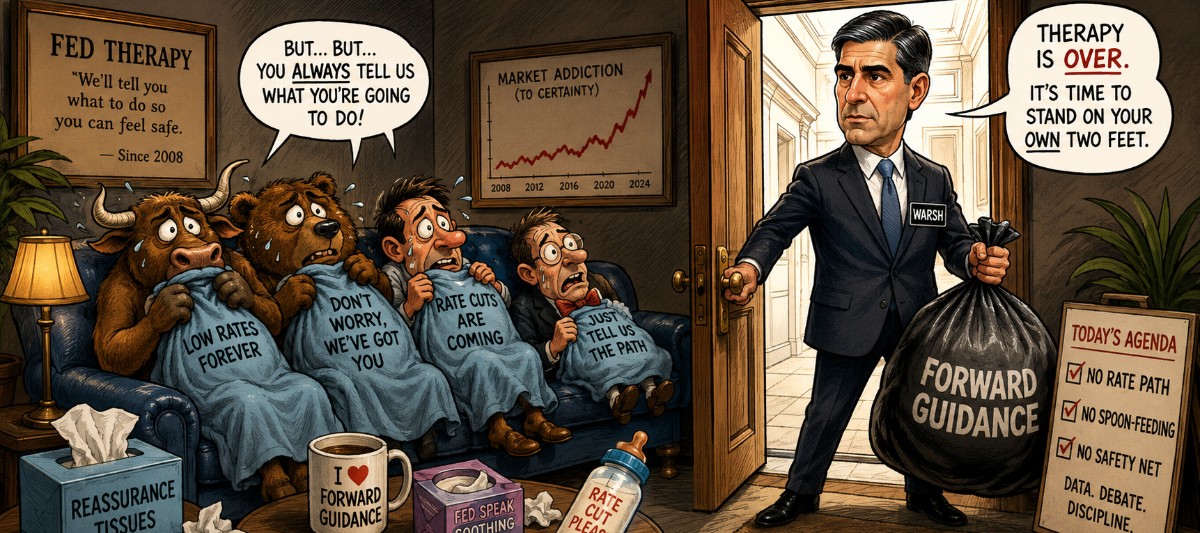

The Fed's Cold Turkey

Posted June 18, 2026

By Sean Ring

Hormuz Premium

Posted June 17, 2026

By Sean Ring

Wuhan Whoopsie!

Posted June 16, 2026

By Sean Ring