Posted June 18, 2026

By Sean Ring

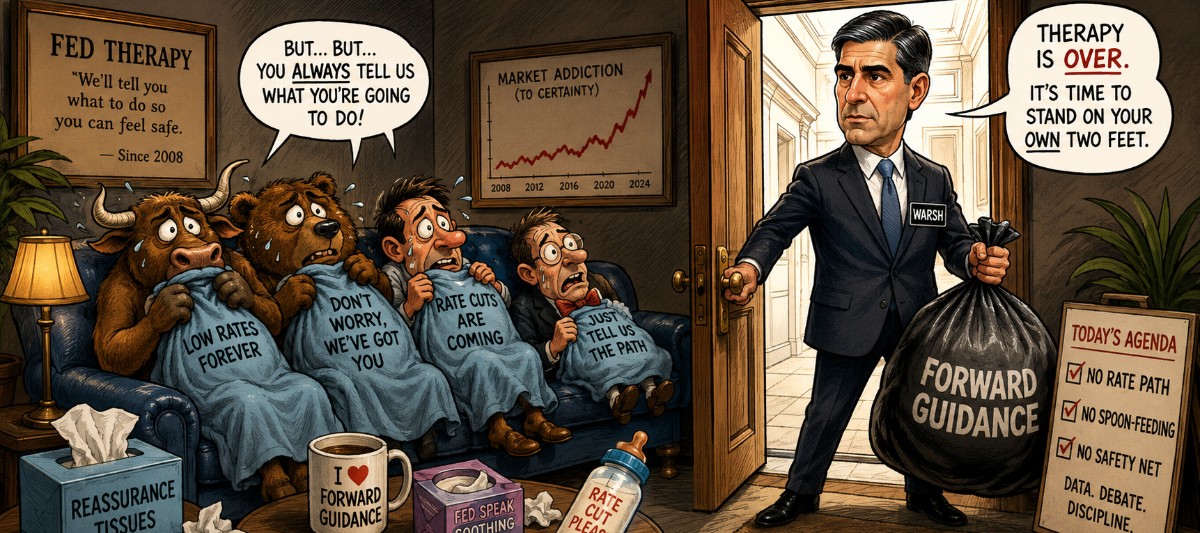

The Fed's Cold Turkey

The security blanket is gone.

For 16 years, investors had a deal with the Federal Reserve. The Fed would tell them what it planned to do. Markets would price it in. Everyone would feel safe. The arrangement had a name: forward guidance. It was cozy, predictable, and wildly addictive.

New Grand Poobah Kevin Warsh just ripped it away.

Wednesday was his first press conference as Fed Chair. He held rates steady at 3.50 to 3.75%. That was the expected part. Everything else was not.

The new dot plot shifted up. A clear majority of officials now pencil in at least 1 rate hike by year-end, not the cuts markets had been quietly praying for. Warsh then stood at the podium and told reporters, in plain English, that he wouldn’t give them a rate path. He said forward guidance is not well suited to the current environment.

Markets heard him. The S&P 500 dropped about 1.2%. The Nasdaq and Dow fell by similar amounts. Small caps got hit harder, down around 2%. The 2-year Treasury yield jumped above 4.20% on the news before settling near 4.18%. (The Fed has more control over the short end of the curve than the long end.) The dollar firmed. Gold sold off by more than 3%.

As one bank economist put it, it was a day when the markets lost a friend.

Good.

The Unprompt

The Unprompt is what I’m calling the deliberate withdrawal of the one thing markets have leaned on since 2008: the Fed’s willingness to tell you what it will do before it does.

Every press conference became a therapy session for neurotic investors. The Fed calibrated its message to avoid upsetting investors.

Warsh is not that. He said the statement simply presents the facts as accurately as we can assess them. He said he wanted a “family fight” inside the Fed, meaning a real debate rather than a pre-cooked consensus. He refused to validate specific market expectations. When asked about the sharp moves in yields and equities, he said he welcomed an “unfiltered market response.”

The man is telling investors to stand on their own two feet.

Why This Matters

Austrian economists have a word for what the Fed has been doing. They call it capital misallocation. When the central bank artificially suppresses interest rates and then tells you exactly how long it plans to keep doing so, it distorts the price of money. And that distorts every decision made downstream.

In this world, businesses, especially Silly Valley start-ups, assume cheap money will last forever and plan accordingly. Investors start to price in cuts that haven’t happened yet. Governments change laws so pension funds can chase yield into riskier alternative investments. Everyone bets in the same direction simultaneously.

Economists call that a cluster of errors. You know what regular people call it? A boom. And you know what follows a boom...

Forward guidance made the boom bigger and the eventual bust more certain. By telling markets exactly what it would do, the Fed allowed the misallocation to run longer and deeper than it ever could in a world of genuine uncertainty.

Warsh is putting uncertainty back into the system. That’s painful in the short term. It’s necessary in the long term.

He Even Said So

Warsh was unusually direct. He told the room that the Fed had fallen short on inflation for 5 years and that “we are going to rectify that.” He said the committee’s commitment to deliver price stability is “strong, unanimous, and unambiguous.” Warsh acknowledged that change carries inherent risks but said progress was possible anyway.

He also made a quiet admission that goes deeper than any rate decision. The prior Fed, he implied, had talked too much. It had strayed into areas it should not have touched. It had laid its cards on the table so completely that markets stopped pricing assets and started just mirroring Fed talk.

That is a polite way of saying the last Fed chair let markets become dependent. Warsh is cutting off the supply.

A Word on Gold

The metals sell-off on Wednesday was not accidental. Gold dropped more than 3% during and after the press conference. Precious metals investors should understand why.

Gold and silver thrive in one specific environment: negative real interest rates. When the Fed holds nominal rates so low that inflation runs ahead of them, savers lose money by holding cash. Hard assets become the rational alternative. The gold bull market of the last several years was, in large part, a story about a Fed that was too easy for too long. That, and the USG’s idiotic decision to weaponize the dollar system, of course.

Warsh is signaling the opposite. Higher rates for longer. A genuine willingness to hike again if inflation demands it. No more spoon-fed reassurance that cheap money is permanent.

That is structurally bearish for gold and silver in the near term. Not because the metals have no value, but because the specific tailwind that drove them is weakening. If you hold gold as a long-term store of value and a hedge against fiscal disaster, the thesis remains intact. If you were holding it as a bet on perpetual Fed easing, Wednesday was a signal to reconsider.

Wrap Up

Most investors are still waiting for the old Fed to come back. They are sitting in positions built around the assumption that any economic wobble will produce a quick pivot to rate cuts and reassuring press conferences. They’re waiting for the adult to come back and tell them everything will be okay.

Warsh gave you a clear answer to how long that wait will be.

He isn’t coming. Markets will price assets off data and dots, not off hints from the chairman’s carefully chosen adjectives.

That is uncomfortable if you were longing for the reassurance. It’s clarifying if you weren’t.

The Fed is not our friend. It never was. Now it has stopped pretending otherwise.

Hormuz Premium

Posted June 17, 2026

By Sean Ring

Wuhan Whoopsie!

Posted June 16, 2026

By Sean Ring

Rockets… and Bubbles?

Posted June 15, 2026

By Sean Ring

The Best Trade Since 1776

Posted June 12, 2026

By Ray Blanco

Feeding the Electron Beast

Posted June 11, 2026

By Matt Badiali