Posted June 15, 2026

By Sean Ring

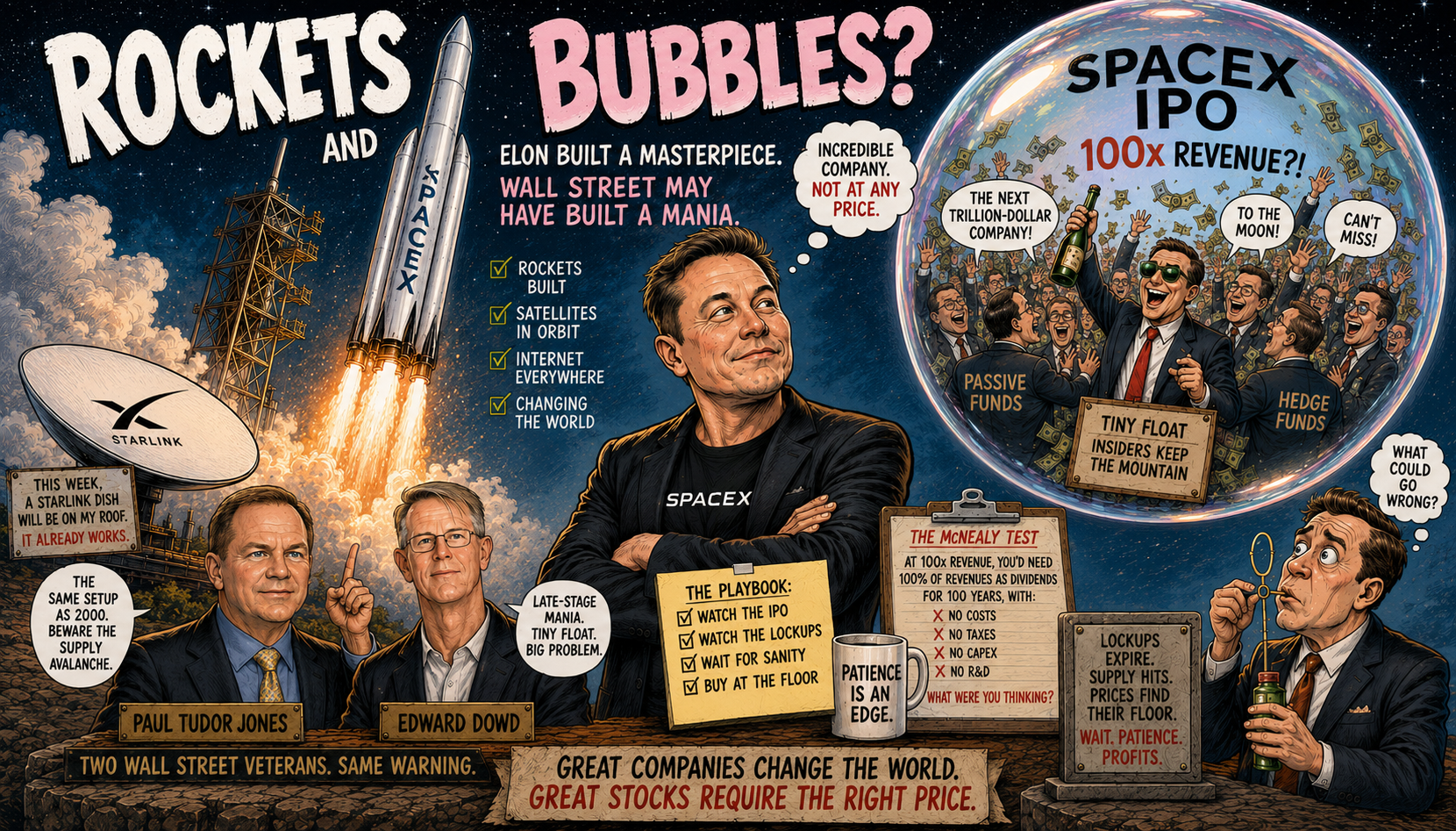

Rockets… and Bubbles?

This week, there will be a Starlink dish on my roof.

That’s because right now it’s in the middle of my front yard. And it still works. Perfectly. My lunatic roofer will ascend Ring Manor’s walls and plant it topside. I sure as heck wasn’t going to.

Without that little white square of a satellite dish, I'd be at the mercy of whatever Telecom Italia had chosen to install… whenever they got around to installing it. Which is to say I'd be staring at a blank screen, still waiting. So I’m eternally grateful to Elon for what he’s done.

Musk put Starlink satellites into orbit. He built the rocket that launched it. He founded the company that made both possible. I use it every day. I'm grateful.

And I'm still not buying SpaceX stock at these prices.

Let me tell you why… and why 3 of the smartest veterans on Wall Street agree with me.

The Bell at the Top

Fellow NBA Champion New York Knicks fan Paul Tudor Jones has been in this business since before most financial journalists were born. He called the 1987 crash. He saw 2000 coming. And right now, he's drawing a direct line between today's IPO frenzy and the one that preceded the dot-com bust.

His argument is the market spent years shrinking its share count. Buybacks pulled stock out of the market. As a result, supply shrank and prices rose. Now, the IPO wave hits. (After SpaceX comes Anthropic and ChatGPT.) Supply will flood back in. The game will change completely.

Jones called the 2000-2002 bear market the easiest bear of his career because it was so clear. We had a boom in new issuance and lockup expirations, followed by a supply avalanche. Prices tanked.

He sees the same setup now. SpaceX isn't just another listing to him. It's a potential inflection point in the supply-demand balance for equities.

Edward Dowd comes at it from a different angle. He spent years at BlackRock. He knows how capital moves. And what he sees today is a classic late-stage mania. AI. Private markets. Innovation brands. All the ingredients of the 1999 cocktail, mixed fresh for 2026.

He sees an IPO at a sky-high valuation with a tiny free float (as Paradigm’s own Gandalf the Gray, Byron King, wrote about last week in the Rude). Retail money, private banking clients, and passive funds bid for a sliver of shares. Insiders sit on the mountain. The stock pops on scarcity. Then the lockups expire, and the mountain moves to market.

Jones and Dowd are saying the same thing in different languages: the spectacular IPO is often the bell ringing at the top. Not the starting gun for safe long-term gains.

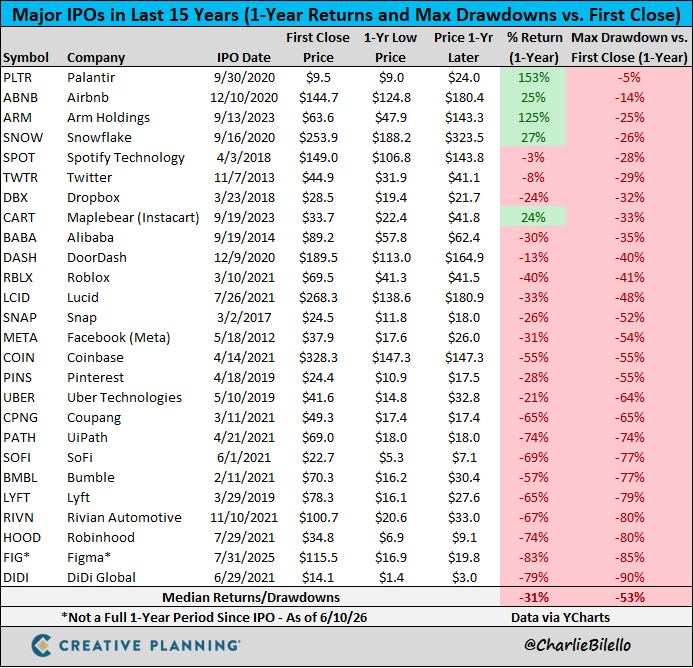

And if you think Jones and Dowd are being old fuddy duddies, feast your eyes on this table from Charlie Bilello:

Credit: @charliebilello

Finally, investor Steve Eisman, played by Steve Carell in The Big Short movie, said, “The valuation's silly."

The investor famously bet against the housing market just before the 2008 financial crisis. He believes SpaceX's future may increasingly depend on artificial intelligence, which could make the business considerably more expensive to run than its supporters are pricing in.

Eisman thinks investors’ expectations are too optimistic.

Optimistic for the Future, Skeptical about the Finance

I wrote about this earlier this year for the Daily Reckoning, but I’ll reiterate it here.

The case study is Facebook's 2012 IPO.

My old friend G, then a Goldman partner I knew from our days at London Business School, was the one who opened my eyes to how the game really works. I remember telling him the Facebook IPO was a disaster. Morgan Stanley had priced it at $38. The stock fell to $17 within five months. Early buyers were carried out.

G looked at me like I'd missed the entire point.

“Failure? For whom?” he said. “Seanie, Facebook raised $16 billion. Zuck never has to go to the market again.”

He was right. From Mark Zuckerberg's perspective, it was a triumph. The company got its cash. The founders locked in their wealth. The bankers took a reputational hit. But the Day 1 buyers got taken to school.

The stock eventually recovered. It became a monster. But that first cohort of IPO buyers waited until August 2013 to break even… if they held on at all.

SpaceX is a far more spectacular company than Facebook was in 2012. That's precisely why the risk is greater. The hype is bigger. The valuation is more extreme. The distance between the story and the numbers is a yawning chasm.

This time, Elon’s got his capital. (Believe me, selling now is anything but unpatriotic since Elon already has all the capital he needs.) His founders will get their cash. Early investors? They may get much less than they bargained for. Yes, Nasdaq is allowing early entry into its index. So those passive funds will have to buy SpaceX. But S&P is not. It’ll be fun to see what kind of divergence develops between the two indices.

The McNealy Test

Scott McNealy was the CEO of Sun Microsystems during the dotcom boom. Sun was a real company. It made real hardware. It had real customers. And it got priced at 10 times revenue (that’s P/S, not P/E) at the peak.

Years later, after his stock collapsed, McNealy explained the math with brutal clarity. At 10 times revenues, he said, you'd need 100% of revenues paid to shareholders as dividends for 10 straight years — with zero cost of goods, zero expenses, zero taxes, and no R&D — just to break even. He asked analysts, "What were you thinking?”

SpaceX was offered at roughly 100 times its revenues.

Run McNealy's test at 100x. To get your money back, SpaceX would need to pay you its entire revenue — every dollar it earns — as a dividend for a century, with no costs. No taxes. No capital expenditure. A hundred years of total revenue handed to shareholders.

Does that sound like a reasonable investment?

I'm cheering for SpaceX to reach Mars. But I'm not giving it capital on those terms.

Great Men, Great Companies, Terrible Entry Points

This is the trap that catches patriotic investors again and again. America produces remarkable companies. Americans love them. They want a piece of the story.

And they should. American enterprise is the greatest wealth-creation engine in history. The country has built more world-changing companies than anywhere else on Earth.

But great companies and great investments aren’t the same thing. The price you pay matters as much as what you're buying.

Microsoft was a magnificent company in 1999. If you bought it at the peak, you waited 16 years to break even. Cisco was running the backbone of the Internet. Peak buyers waited longer. Qualcomm, Intel, Oracle — real businesses, real products, real profits — all took a decade or more to recover.

Pop quiz: how long did Nvidia languish before its historic run? Nearly 20 years.

The companies were great. The entry points were not.

SpaceX is a magnificent company. Elon Musk is a once-in-a-generation builder. Starlink is transforming connectivity for hundreds of millions of people. Falcon 9 is the most reliable orbital launch vehicle ever made. If it works at scale, Starship changes the economics of space entirely.

None of that is in dispute.

What’s in dispute is the price.

What To Do

Let the fund managers pay for their seats.

There is a class of institutional investors that will buy SpaceX at any price. They have to. They manage hundreds of billions of dollars. They need to own the defining companies of the age, or they look bad relative to their benchmarks. They don't have the option of waiting.

You do.

The playbook here is simple. Watch the next few weeks. Watch the lockup expiration. That's when insiders can sell. That's when the supply hits. That's when prices historically find their floor.

If SpaceX is the generational company its supporters claim it is, it will still be here in 18 months. It will still be launching rockets. Starlink will still be beaming internet to rooftops around the world.

The only thing that will have changed is the price.

Patient investors have been rewarded in every previous cycle. The ones who waited 6 months after the Facebook IPO bought in at $17 and rode it to investor heaven. The ones who waited for Cisco, Microsoft, and Amazon after the dot-com crash built genuine wealth.

Patience isn’t pessimism. Patience is one of the few edges a small investor has against the institutional machine.

Wrap Up

I want SpaceX to succeed. I want Elon to get to Mars. I want Starlink to keep working so I can write to you from wherever I happen to be on this planet.

But wanting a company to succeed and wanting to buy its stock at any price are two different things.

Jones and Dowd warn that the IPO wave may be the bell at the top. Eisman, along with almost every other investor, thinks SpaceX’s valuation is insane. History shows that the greatest companies at the highest valuations make the worst entry points.

Let the big funds fight now. Watch where the lockup expiration lands. Then, if the price has come into something resembling sanity, consider building a position. And to remind you, Elon already has all the funds he’ll need from the market to build his dream.

The rocket will still be flying. The dish on your roof will still work. And you'll have bought in at a price that leaves room for you to actually make money.

The Best Trade Since 1776

Posted June 12, 2026

By Ray Blanco

Feeding the Electron Beast

Posted June 11, 2026

By Matt Badiali

The Rivets Behind the Rocket

Posted June 10, 2026

By James Altucher

One Small Float for Man

Posted June 09, 2026

By Byron King

The Philly Hangover

Posted June 08, 2026

By Sean Ring